Lending Club DD

Lending club is an unloved and attractive stock for a re-opening play with a great growth story and big vision. I belive it is nice long term play.

On this blog, I typically don't do analysis of individual stocks. However, I do feel LendingClub deserves some love and it is a very misunderstood business.

Lending club initiated as a peer-to-peer lending marketplace. Turns out this was not a great business model to have individual (retail) investor lend to other retail investor. The main issue was friction, the time to get the funding and the availabilty of funding. In december 2020, they shut that down and will focus on getting institutional money to fund the retail loans.

Catalyst

Lending club announced they were acquiring a bank. This was early 2020. It was the first time since 2008 that a fintech acquires a bank. In my opinion, acquiring a bank is genius since it will do the following :

- Save 40m$/ year in funding fees they currently pay to banks.

- Easy access to liquidity (deposits from Radius bank users)

In terms of financial, it looks they are on the right track.

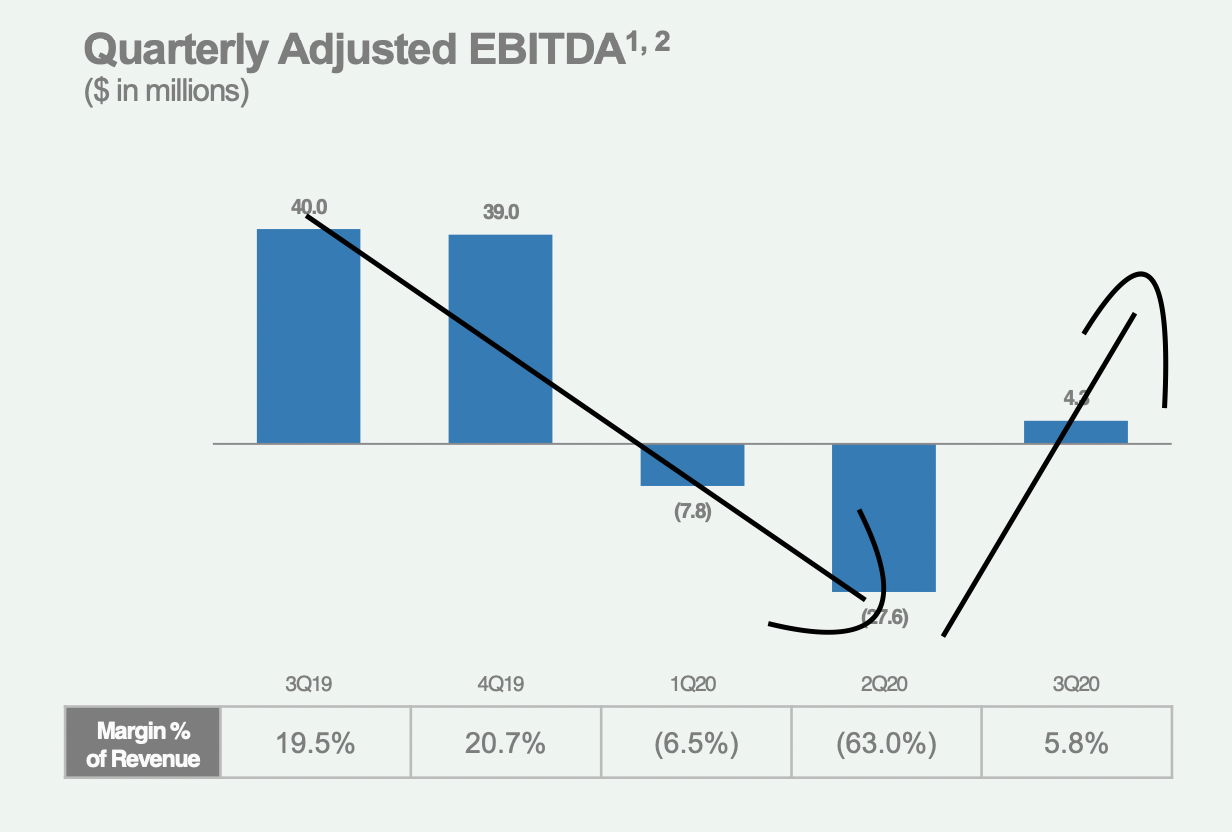

In the last quarter before the pandemic, they managed to turn a profit on a EBITDA basis (about 4.3M$)

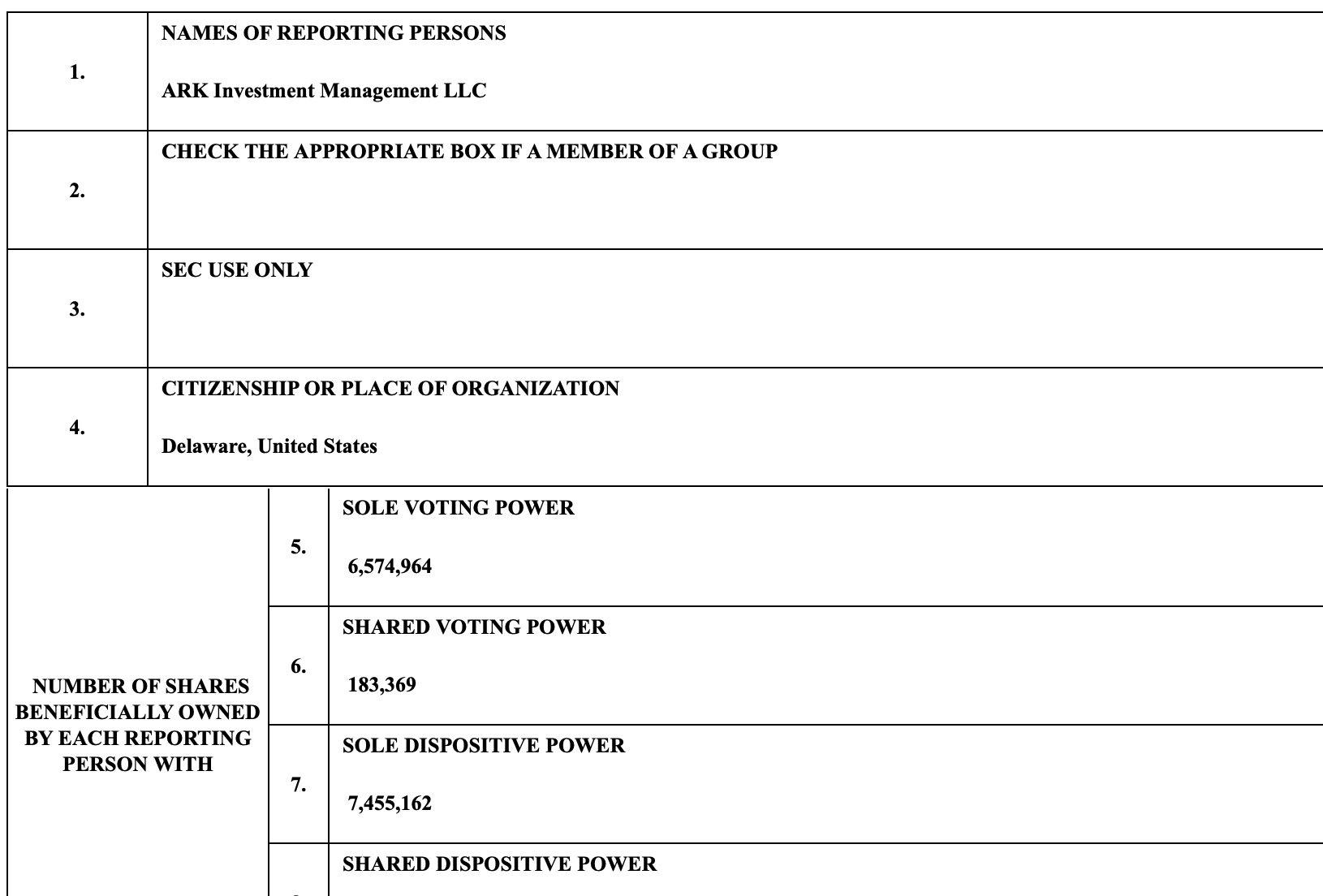

The biggest shareholder of Lending Club is ARK Invest. They both 8% of the company which is the maximum their fund allows them to do.

Finally, valuation is quite attractive. They are trading below their entreprise value of ~950M$. They have 570m$ in cash in the bank (before Radius bank acquisition)

Vision

Buying Radius bank will allow Lending Club to become a true marketplace with fintech on both sides. Radius bank is what we call an open API banking banks. Lending club now call themselves a NeoBank.

One of the main issues with fintech is acquisition cost (as it is for the banks). Banks can afford those expensive credit card promotions with their cash flow. However the acquisition cost for fintech is high and without steady cash flow, it impacts their balance sheet significantly.

For an up and coming fintech, this is a win-win since instead of the paying extra acquisition cost, they can simply hop on the lendingClub marketplace and compete for business. Their only acqusition cost is paying Lending Club a fee (only if the customer takes the loan). So they can focus at what they are the best at, underwriting loans.

It is also a win-win to Lending Club, since they can send the loans to multiple underwriter and get the origination fees.

Finally it is another win-win for the customer since they just need to apply for a loan once and get multiple offers at different prices.

Note that this vision is still speculation at this point, but if Lending Club is able to execute properly, this could happen within the next few quarters. And Lending club is very well position to take advantage of this.

In summary this is a winner-take-all approach where fintech firms get business for cheaper than current acquisition costs and lending club makes money as well. In this setup, everyone involved wins, the fintech firms, lending club and the consumers.

In summary this is a winner-take-all approach where fintech firms get business for cheaper than current acquisition costs and lending club makes money as well. In this setup, everyone involved wins, the fintech firms, lending club and the consumers.

I am not a very savvy technical analyst (I usually suck at technical analysis and it seems that all my trade are never as great as they could be), but I mostly rely on my vision on what a business potential it has or could be.

They are reporting earnings on March 11th 2021.

Fairly valued re-opening play:

At this point, there are only a few not so overvalued re-opening play available in the market. I would argue Wells Fargo, Exxon are but these are big companies and potential upside is 2x at most. I wouldn't hold them for the long term.

Uber and Airbnb are amazing re-opening plays (with no debt) and potential to become trillions dollars valuations but they currently fairly valued (Airbnb is definitly priced for a lot of growth).

This is where Lending Club comes in. Right before the pandemic, it has about 40M$ in EBITDA.

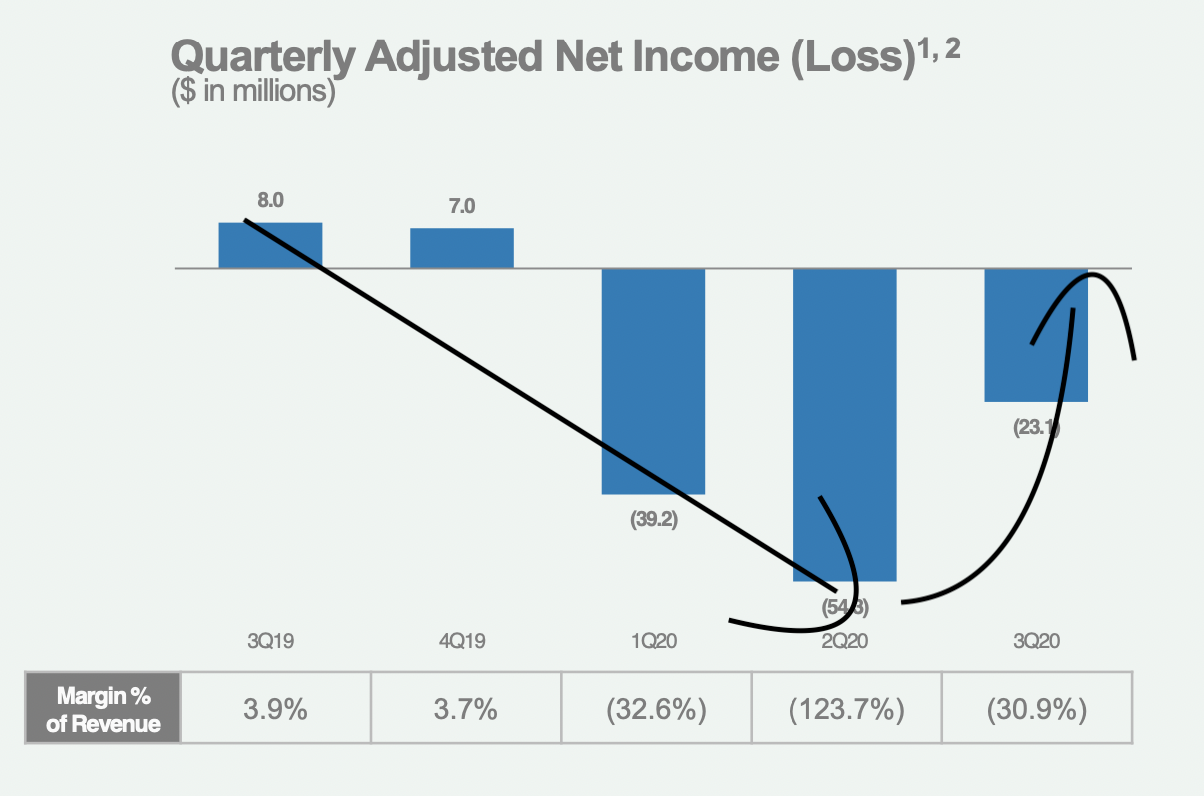

Same trend with the GAAP net income :

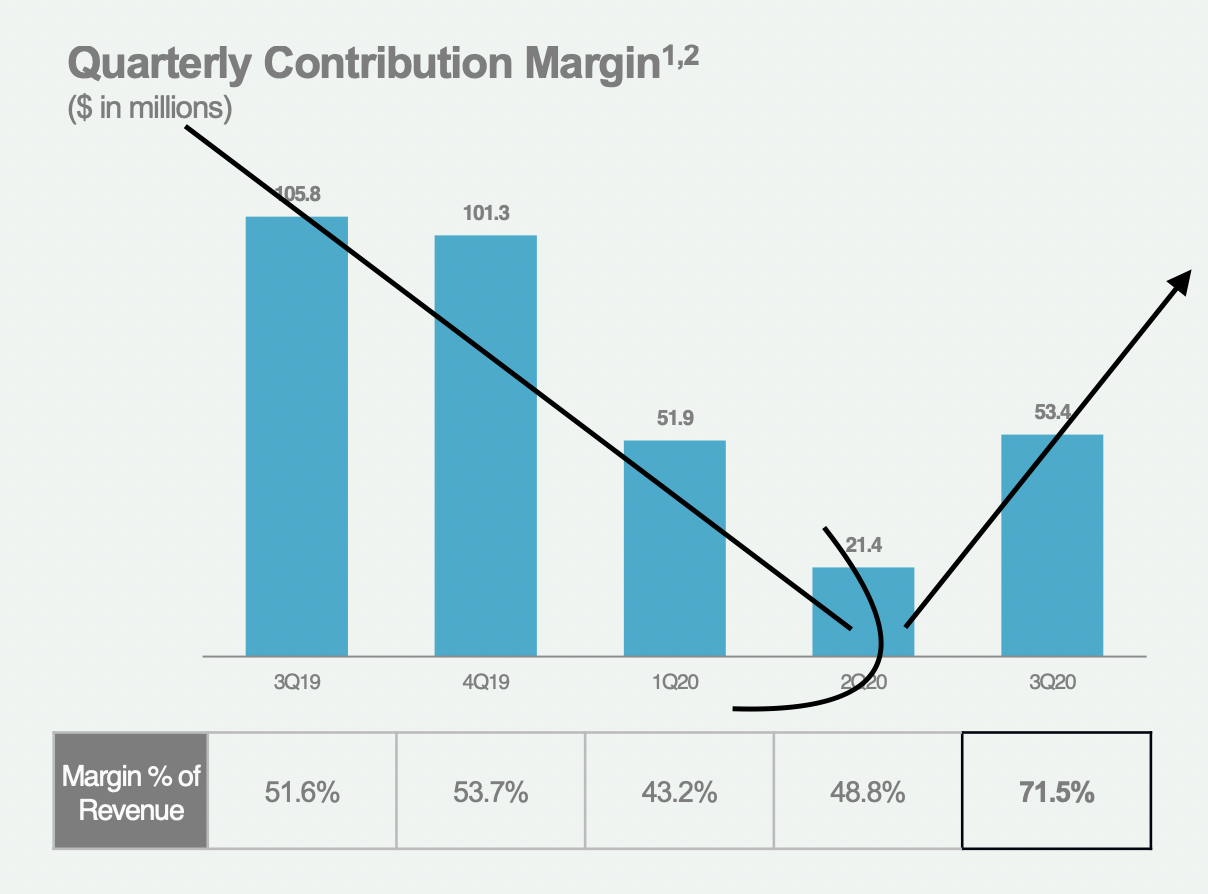

My assumption is that they will be able to return to this level and this is even without counting the cost saving they have accomplished during the pandemic (30%). Remember, $LC is a platform company, so the cost of servicing extra loans doesn't increase linearly. You can see this with their contribution margin impact. They are now able to achieve higher contribution margin than before the pandemic started:

Of course, during the pandemic, most americans couldn't spend money (or get into debt) with an economy that could collapse at anytime. This was a bad global macro-environment to operate a unsecure-lending platform. However, the consensus is that the worse is behind us.

Finally, I will use an annualized net income for Q4 2019. I do believe this is a pessimistic number since it does not include the cost saving of 2020 (30% layoffs) and the cost savings of Radius bank. Q4 2019 had a net income of 8M$ which I will use 32M$ as future conservative estimation for annualized income.

This gives a multiple of ~30 P/E (950M$/32) and P/S of (204M$* 4)= 808M$/950B$ = 0.85 P/S.

If you remove the cash on balance sheet, those multiples become extremely attractive (950M$- 580M$) :

- Forward P/E : (370M$)/ 32M$ = 11.56

- P/S : 370M$/ 808M$ = 0.45

With the cost savings done during the pandemic, I believe they can achieve better. And note that this doesn't include the Radius Bank acquisition cost saving stated above. However Radius bank is a private company and that is a wild card (we don't know how well this business is ran).

I strongly believe the re-opening play is a once in a lifetime opportunity. It is unheard to have all the major economies of the world in sync about to unlesh a hoard of consumers trapped in their houses for the last 16 months.

I strongly believe the re-opening play is a "once in a lifetime" opportunity. Or at the minimum this IS the play of this decade.

Cathie Wood factor

And to add to this, ARK invest owns ~8% of lending club. I am a big fan of ARK invest, but a lot of people follow them so they move the market for some stocks. Lending Club however, remained an obscure holding at the bottom of their portfolio since it accounts for only about ~100M$ (out of a 58B$ Asset under management).

https://www.sec.gov/Archives/edgar/data/1409970/000110465921024165/tm216840d1_sc13.htm

ARK invest endorsement is key since it signifies that Lending Club is a growth company. ARK only invest to capture a 20% annualized compounded growth. In my opinion this is one of the rare growth and value stocks out there.

In my opinion this is one of the rare growth and value stocks out there.

Summary:

In summary, I like the stock ($LC). A few catalyst are on the horizon for 2021. It won't be an overnight success, but if they keep executing the future is bright for them.

- Radius bank acquisition.

- Ideal reopening play

- Attractive valuation for annualized pre-pandemic (Q42019) multiple minus net-cash of ~11 P/E or 0.45 P/S.

- ARK invest owns ~8% of $LC

Disclosure : The author owns this security in his portfolio. He was dumb/retarded enough to buy at IPO and kept buying all the way down to lows of 2020. He finally managed to DCA (Dollars cost average) out and as of Feb 20th, his positions have a slight miniscule profit. But he has no plans on selling anytime soon and this is a 5+ year hold. This post is only for entertainment purposes, I am not in no-way/shape or form remotely qualified to provide any financial guidance or advice.

Subscribe to Be free and wealthy blog

Get the latest posts delivered right to your inbox