Is GoPRO $GRPO a turn-around story in the making?

$GPRO has been left for dead.

From the high of the IPO of market cap of upward of 10B$ to now a merger ~235M$ MC.

It's an interesting company.

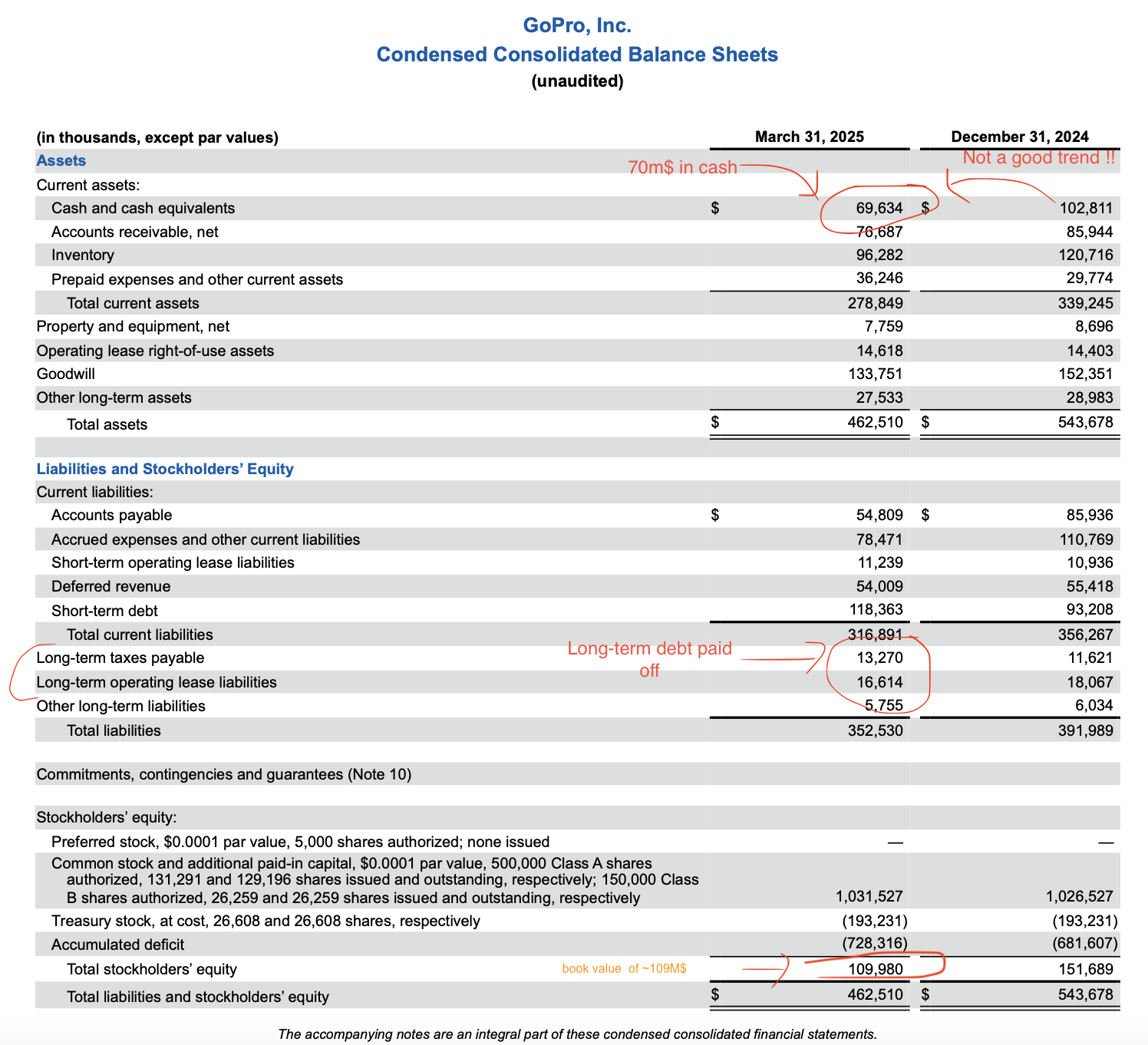

- No Long-term debt

- ~70M$ in cash as of last quarter.

- Book value : ~110M$

- Market cap : ~238M

- EV = 238M$ - 70M$ = 168M$

Let's dive into the balance sheet:

So book value is around 109M$. It's not often that the market give you opportunities like this one.

Peter Lynch famously said : "A debt free company can't go bankrupt."

https://x.com/QCompounding/status/1946147306362880299

The question is how is the rest of the business worth.

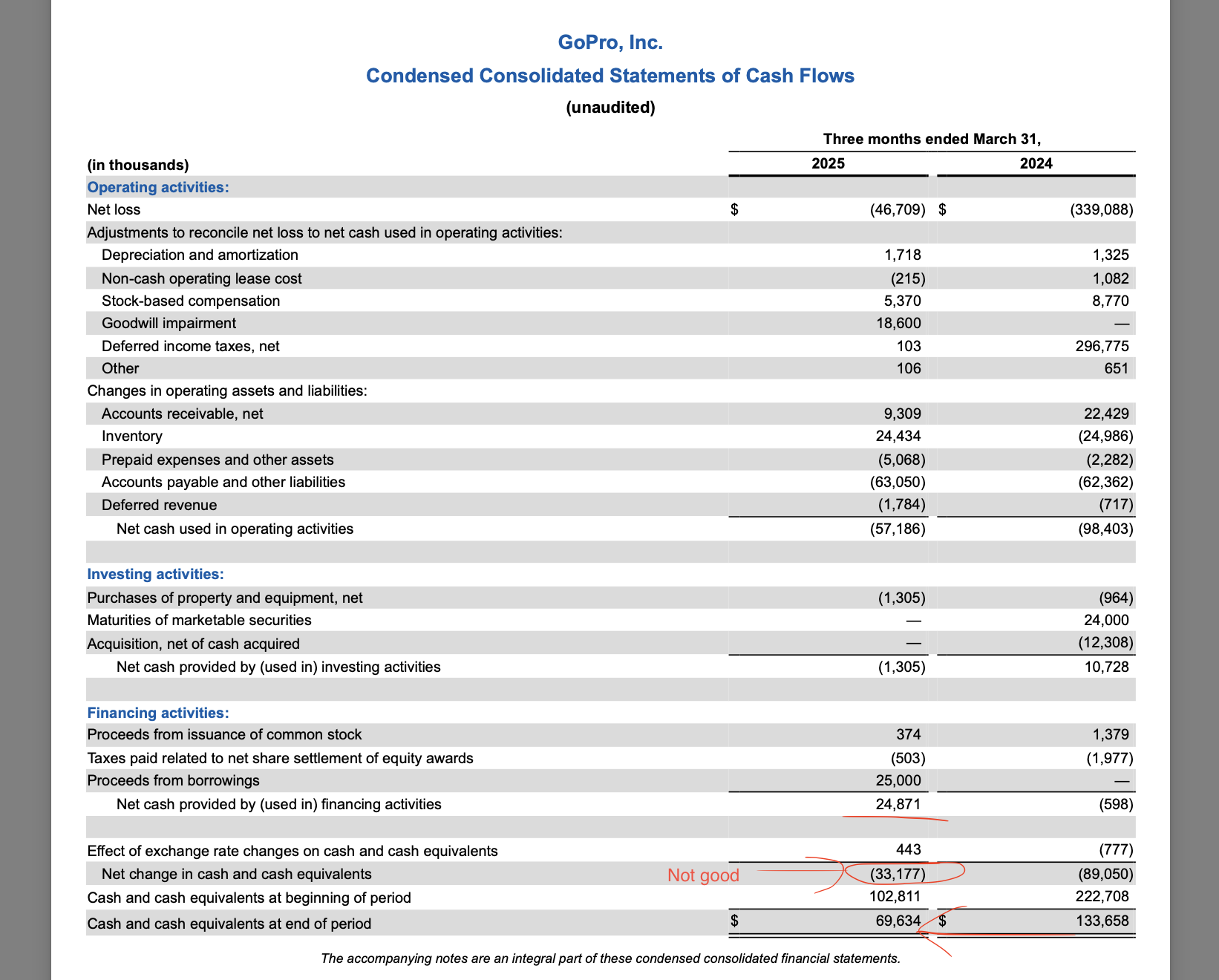

They still have a problem where they are burning throught their cash.

Estimating the value

Current EV is around 168M$. Let's stack up if this makes sense.

-

IP / Technology :

That part is a bit hard to evaluate but let's put a number at around ~50M$ to be conservative. 50M$-100M$ range is quite common for pre-revenu companies. -

Brand :

GoPro is a globally well known brand. This is probaly the most valuable part of the current business. I would easily value this at 100M$. -

Inventory/ Hard assets:

PPP : 7M$

Point-of-Purchase display : ~13M$ -

Value of recurring revenues

They currently have 2.57M subcribers at 49.99$/year.

That's 125M$ ARR yearly. Assuming some meager growth, this brings it up to 200M$ ARR in 2030.

What would be the present value of that yearly ARR? Average would be 5x revenues, but let's be conservative and only use 1.5x revenues : ~187M$.

So at current trading value (1.5$), it may be properly priced, but those would be fire price sales.

This blog would argue that it appears there are some value.

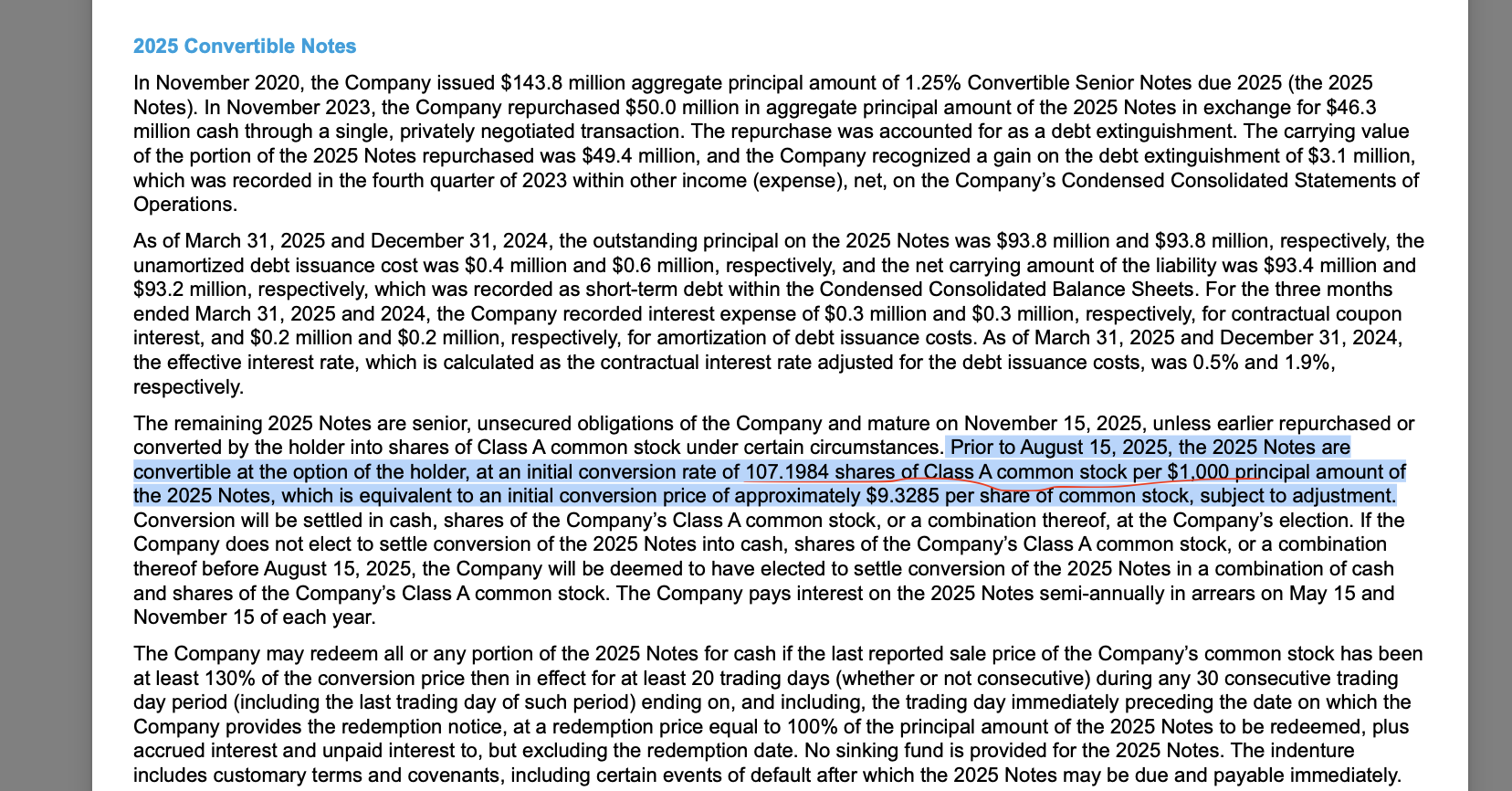

Convertible notes

There are August 2025 convertible notes expiring. This will create some extra dilution. The conversion price is around 9.33$/share

at an initial conversion rate of 107.1984 shares of Class A common stock per $1,000 principal amount of

the 2025 Notes, which is equivalent to an initial conversion price of approximately $9.3285 per share of common stock, subject to adjustment.

Bull case:

With current boom in AI, having the HW to be able to capture videos and then process it in the cloud, there must be a good story here.

Just take the Jony Ive company that got sold to OpenAI, which may be just a fancier, smaller GoPRo.

Challenges

They definitely have challenges.

They are losing about 0.30$/share (when the stock hit a bottom of 0.39$/share.

They need to start growing the business again.

Competition is very agressive (Insta360).

It seems it would be hard for this company to go bankrupt but a more realistic outcome would an acquisition of some sort.

$GPRO is highly speculative but it seems the risk/reward here seems attractive.

This is not investment advice.

Let me know what you think.

Subscribe to Be free and wealthy blog

Get the latest posts delivered right to your inbox