The Opendoor opportunity : Part 3 - iBuying in focus

The idea of iBuying is still a fringe idea by any means. Overall market share is less than 0.5% of all US residential transactions. But it is powerful idea since most middle class families have most of their net worth tied in their primary home.

I believe this space is still one of the biggest opportunity in the market which marries tech and finance together. It allows you to create a strong moat due to regulatory capture. Best examples of great companies executing are Robinhood ($HOOD) and Coinbase ($COIN).

This post will deep-dive a bit more into the iBuying opportunity. Here are my key assumptions :

- 5.3 millions RE transcations. Current real-estate residential is currently frozen due to high rates. So let's use 2019 as the baseline of 5.3 million US residential transacations. Even though I believe it is too conservative since there is a lot of pent-up demand for housing.

- Opendoor can capture 1% to 2% of total US market.

- There will be always consumers that need the money now and don't want to deal with 3-6 months of uncertainty. Think of a family moving coast to coast for a job and they need to buy a new house with their current home equity.

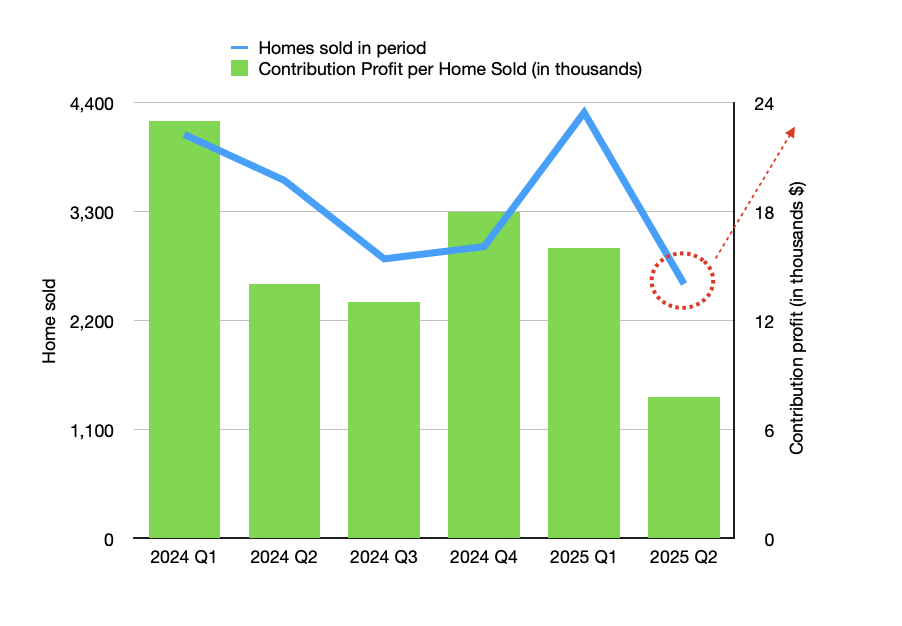

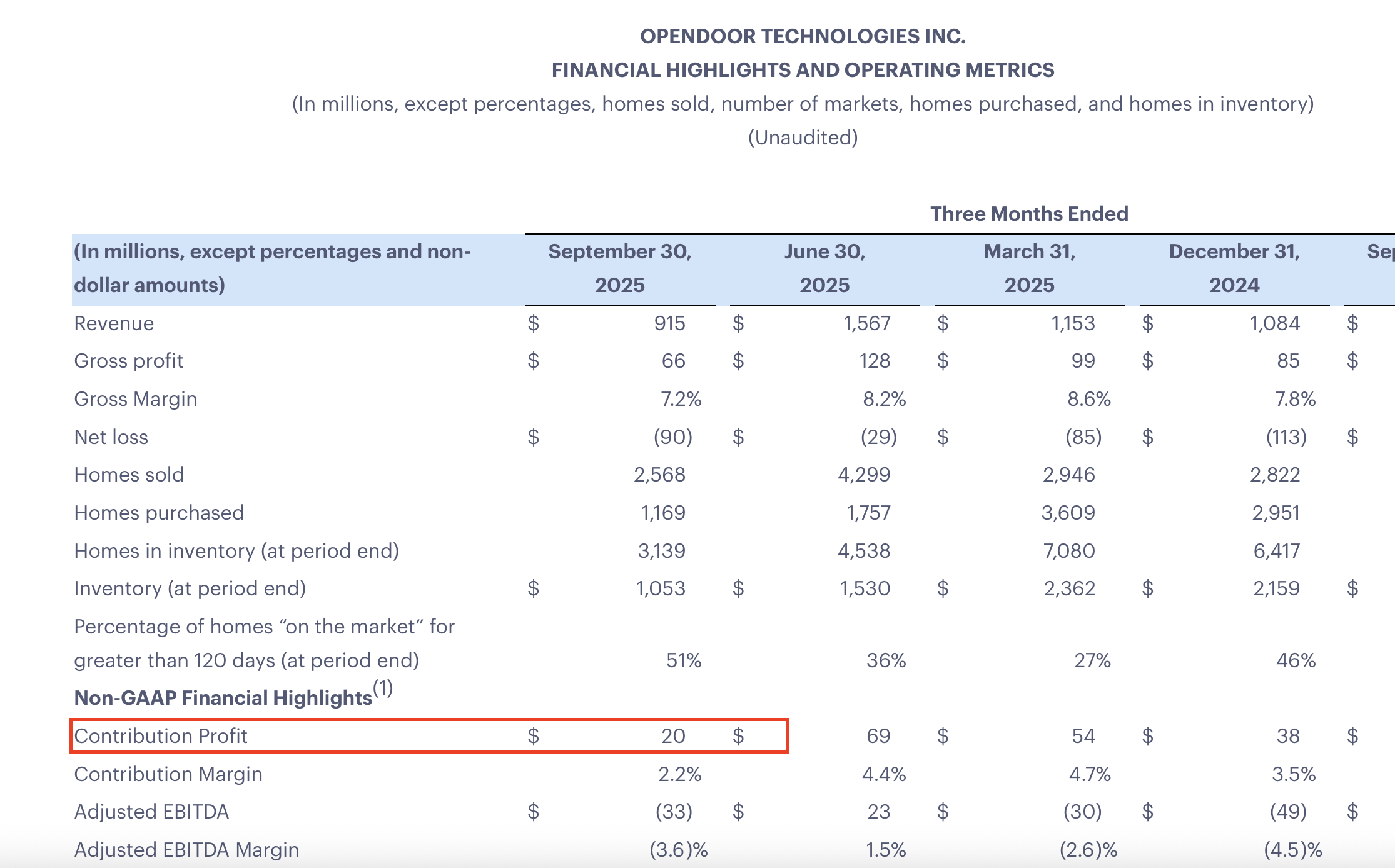

This is the current contribution profit from the last few quarters :

In my opinion, the most interesting metric is the contribution profit. From last quarter, it came at 20m$.

Let's take a look at a simplified model. The main variables are the following :

- The RE transaction goes back to normal (let's take 2019 number of transactions at 5.3m$)

- OpenDoor market share in US. Base case would be 2%

- Contribution profit per house. 16k$ is a conservative and in-line with past quarters.

- Extra services per house. This is the big opportunity. We put in around 3k$ per house, but it could be a lot more.

In honor of Eric Jackson, my base case also ends up very close to 82$. As of last friday, it closed at 6.5$, so the there is quite an assymetric risk profile for this company. But as long term holding and assuming the team executes properly, this stock can go to 250$+ in a few years.

As a disclosure, we are long this stock and we feel comfortable buying the stock at the current levels (not investment advice).

All green cells below are inputs or assumptions. We are using 30x contribution profit for market cap valuation. This may be conservative (for a fast growing company).

Have a great weekend everyone!! $OPEN army strong!

Subscribe to Be free and wealthy blog

Get the latest posts delivered right to your inbox