Reasons to refinancing your mortgage

In this post, I will show you where you can save money on one of your biggest expense: Housing.

I will show you have to save up to 3000$ when doing a mortgage refinance. Explain the pros and cons of refinancing.

Federal fund target rate has been cut to literally 0% (0% to 0.25% to be exact).

I am currently in the process of refinancing my house and I think you should consider first. The beauty of having a mortgage is that your costs are fixed (as opposed to being a renter). If you are a renter, now is a great time to consider investing to become a landlord, but that discussion will be for another post. In this post, we will focus on how a current homeowner can save with refinancing.

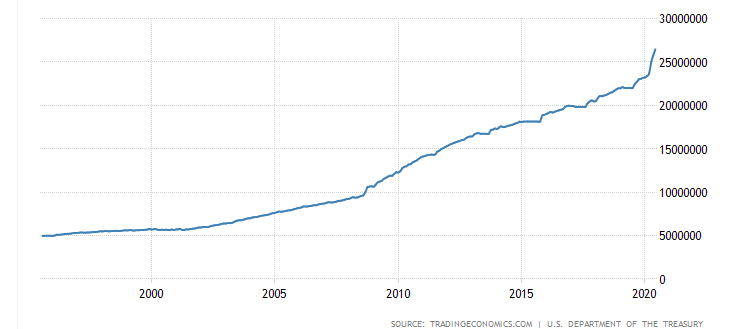

First of all, I need to lay down a few assumptions. Even though we are in a depressionary environment, the US debt has increased by more than 30% just in the last 6 months.

US Debt:

Our current debt has been increasing a faster rate since the Obama administration (by both parties to be fair, I'm not trying to be partisan here). Just take a look at this graph:

There are a few ways to pay down this debt.

- Goverment starts taxing everyone more (very politically unpopular)

- Goverment starts a very aggressive austerity program. Same very unlikely politically.

- Use inflation to eat away this debt.

My guess is that with this amount of printed money and increased in debt will bring inflation. Probably not this year or next, but in a 5-10 year period, inflation will be needed to be able to manage this debt.

Peter Schiff has a good view on inflation. This is the interview with Joe Rogan for 3 hours

Why does this have to do with mortgage rates?

Locking long term debt (like 30 years) allows YOU to make a bet against inflation. With interest rates so low, it should be a no-brainer that taking on long term debt with fixed rate means if inflation goes up, servicing your debt becomes easier.

Along with protection against inflation refinancing have a few more advantages:

Pros :

- Lowering your payments: I am able to save about 1000$/mo just by refinancing. This can be accomplished in 2 ways:

- Lowering your interest rates

- Resetting the payment schedule to 30 years. I'm currently into my 7th year of my mortage. I can take the remainder of my principal and instead of paying it over 23years, I can move it to 30years. My bet here is that inflation will eat away this debt.

- You can take cash out to prepare for an eventual downturn (make sure you have enough liquidity). You could also take money out (at ~2.5%) and invest it in the S&P instead.

Pros:

- Non-recourse mortgage: If your mortgage is the initial mortgage for a few states (like California), your mortgage is non-recourse. If you refinance, it's still a grey area, so it's unclear.

A non-recourse mortgage means if for whatever reason you don't or can't pay, you can walk away and the bank can only take your house (even if you have the remaining money left in the bank). Basically your downside risk is limited (the max you can lose is your downpayment), but the upside is unlimited. These are the kinds of assymetric risk/gain investors like.

For example in California, this is written into law . Check out California Code of Civil procedure section 580b.

No deficiency judgment shall lie in any event after a sale of real property or an estate for years therein for failure of the purchaser to complete his or her contract of sale, or under a deed of trust or mortgage given to the vendor to secure payment of the balance of the purchase price of that real property [...]

So the law is very clear on this topic.

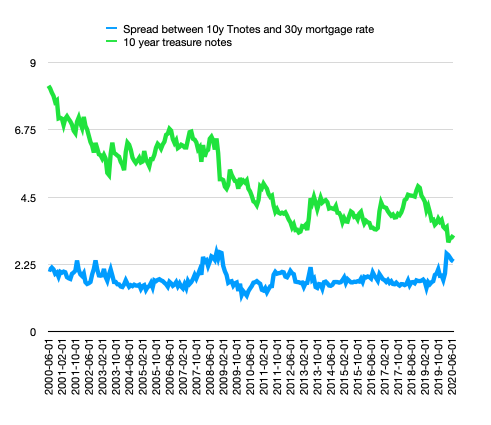

Mortgage rate forecast:

When looking at the spread between the 10year T-Bill and the 30 years mortgage rates, we can see a big spike since they started lowering rates in March. In general, this trend should follow and revert to the mean, so we should expect rates to keep going down.

Shop shop shop:

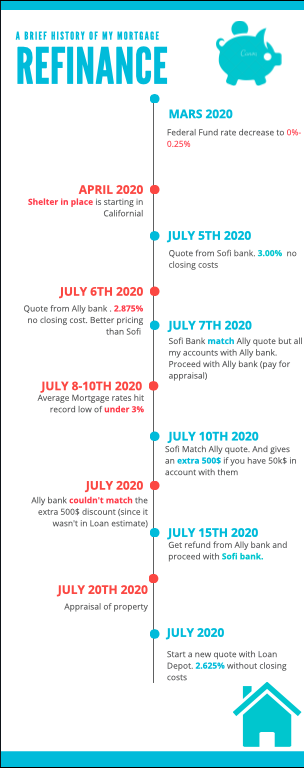

Below is a timeline of my process. This is still a WIP. I will provide an update once this is completed.

The best rate I have hit so far is from Loan Depot with a 2.25% fixed over 30 years. My loan is a 700k$ and my loan officer was pretty good. He was the only one able to waive my appraisal (all other tried but none could).

You can use this referral to use the same loan officer:

The downside of shopping is:

- Time. It does take time

- Credit hit.

- Everytime a lender does a credit hard pull it affects your credit score. Even though this happens through an opaque algorithm, in my case, I had around a ~20 points drop. The good news is that you have a window of 14 days to shop as many as you want before the drop gets registered. So make sure to do your shopping with lenders within that 14 days window.

Why buy mortgage points?

If you plan on keeping your real estate for a longer period (more than 3 years), it makes sense to buy mortgage points.

The only reason not buy points is if you expect to refinance within 1-3 years.

There are 2 main reasons you would want to refinance:

- Investment of 15%+

- Tax deductible but amortized over the life of loan.

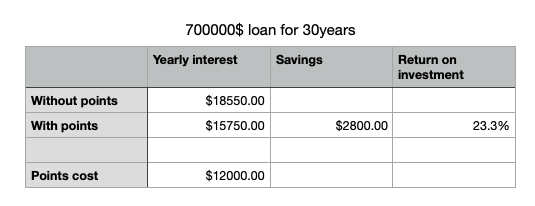

Great investment:

Consider my loan offer. My total loan is 700k$. I can pay 2.625% or if I "invest" 12k$, I can lower this to 2.25% and save about ~2.8K$ per year in interests. This means a ~23% return on my investment. Not bad.

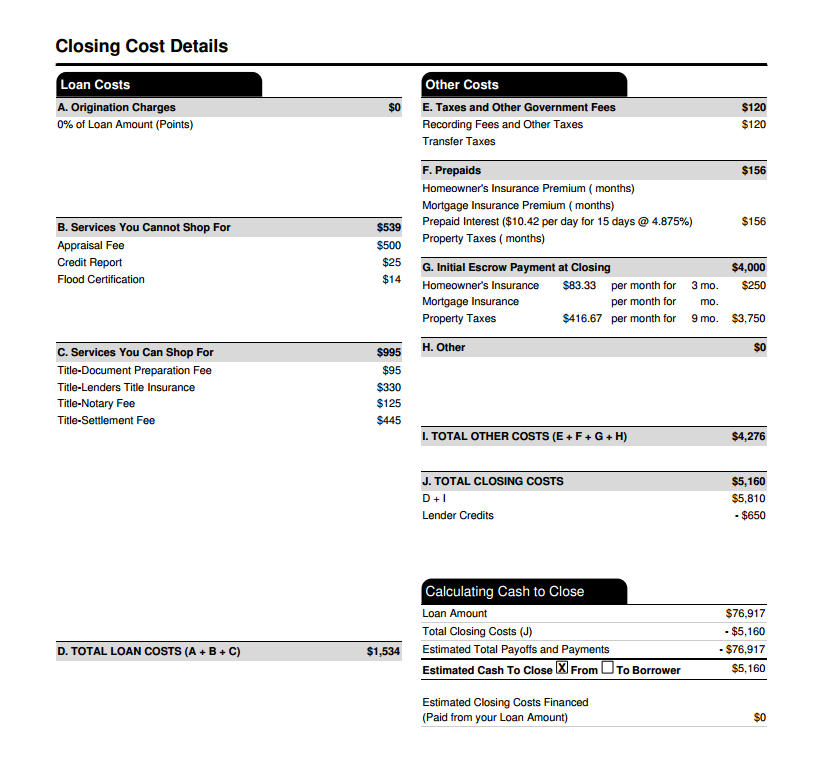

Fee breakdown for mortgage refinancing

Below is the breakdown of all the fees, and how to avoid them.

You will get a Loan Estimate which is standardized. They will all look the same.

Save 600$... waive your appraisal

Apparently most refinance need an appraisal even if you have plenty of equity in your loan. However, turns out to get an appraisal waiver the value has to be less than 1M$ and you need enough equity. As soon as the value goes over 1M$, an appraisal is mandatory. In my case, the propery I was looking to refinance had a value of 2M$, but by using 999k$ as the value I was able to save ~650$ (which is the cost for doing an appraisal).

For the other costs, the best way is to shop around and have lenders compete for your business. I haven't found an easy way to get rid of costs.

I used Loan Depot and was able to get a 500$ lender credit per referrals up to 2500$. I had a very good experience with them and I would recommend them. If you are good at referring friends, then this can help reduce some more costs.

I hope this post was useful. Please share you experience. Of all the bad things that happened in 2020, low mortgage rates is probably one of the few silver linings.

Subscribe to Be free and wealthy blog

Get the latest posts delivered right to your inbox