LendingClub DD update

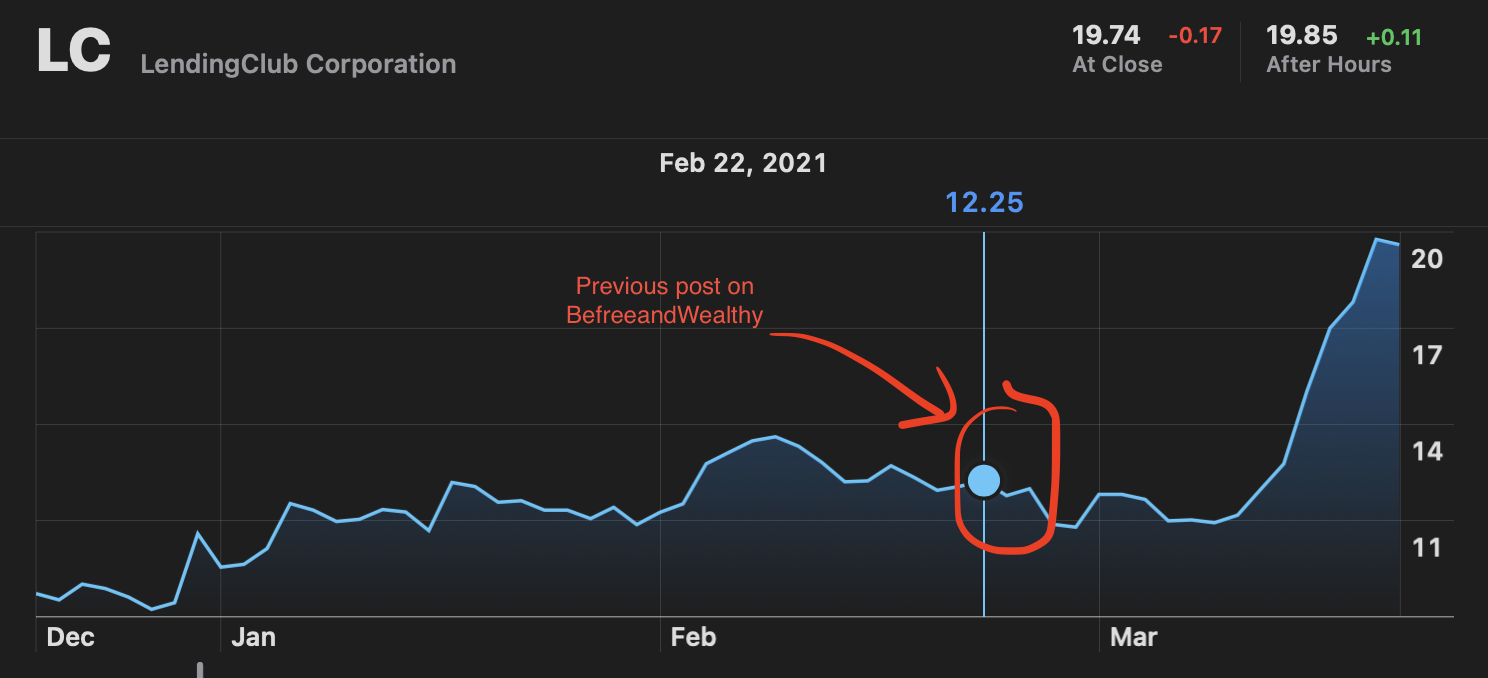

It has been a while ride. Lending Club is up 65% in the last month and back down to the 13-14$ range.

The previous LendingClub DD was about 1 month ago. As a reminder, this is not investment advice.

The main catalyst were :

- Fourth quarter Earning report 2020

- First quarter Earning on April 28th 2021 (including Radius Bank first numbers).

- Ark investment stakes.

- Reopening trade in play, 10Y treasuries going to 1.75%

However this rally appears to be mostly fuelled by institutional money. In this article, I will re-iterate the long term vision of Lending Club and how it can achieve a turnaround.

$LC has the potential to have multiple moats

Warren Buffet famously talked about moat in business and why those are the best investments. In my opinion, lending club was able to build a huge moat around it's business. And surprisingly, no one seems to have paid any attention to it. There are in fact 3 moats surrounding it's business:

- Moat 1: The first fintech (since 2001) to have a banking license (with the acquisition of Radius)

- Moat 2: Data advantage : 15 years of data on 3.6M loans.

- Moat 3: Marketplace platform play

Moat 1: Bank license

The banking license is allowing Lending Club to reduce greatly the origination fees. They are expecting about 30M$ in saving for every 1B$ in deposits. In the latest earning, they implied they have about 2B$ of deposit in Radius bank.

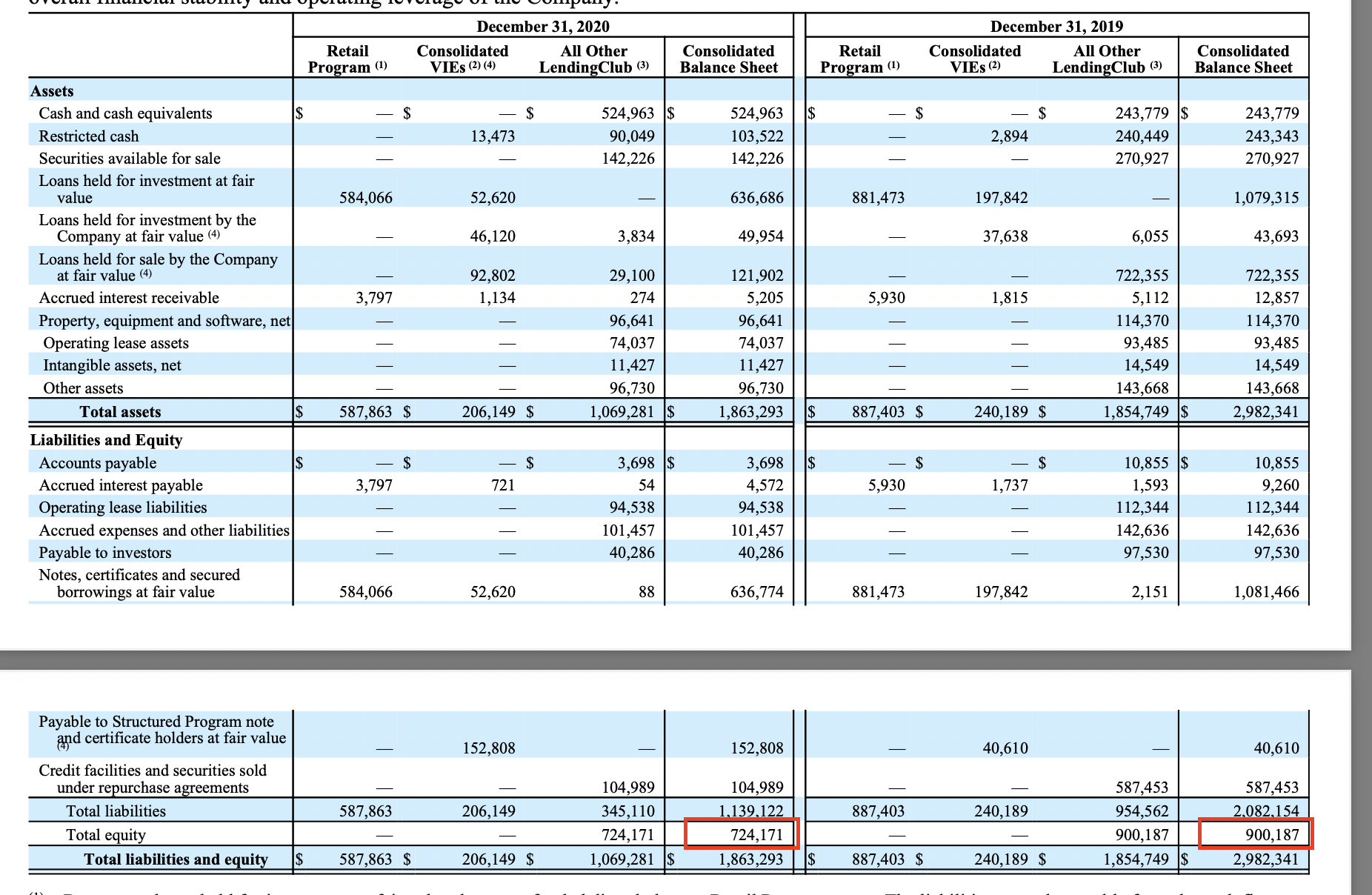

Total asset held by lending club.

If we only look at the current balance (without Radius), $LC stands at around 724M$ in assets:

The balance sheet tells us 2 things:

- $LC business held up pretty well during the pandemic

- $LC is well capitalized versus it's actual assets.

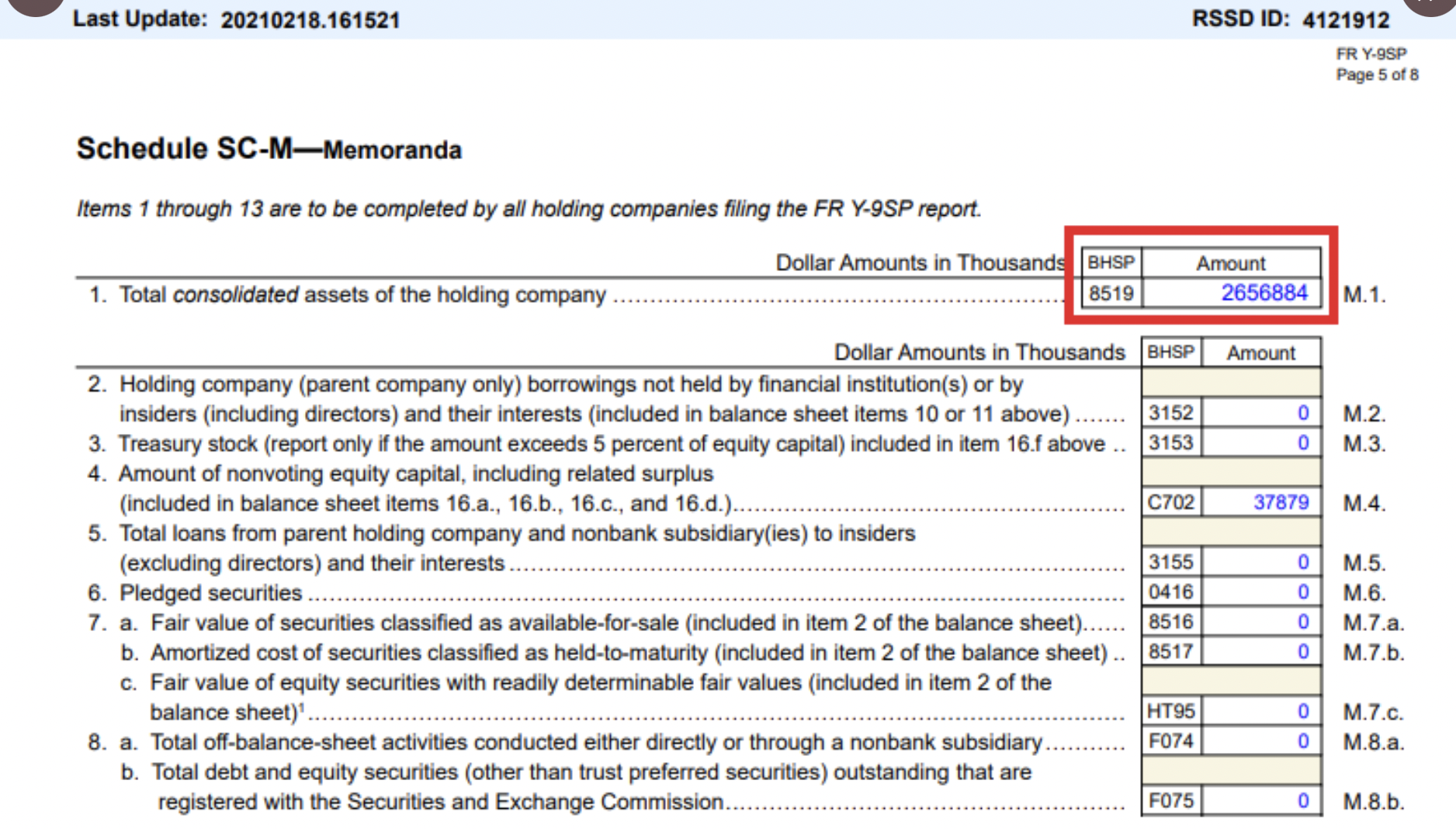

But surprisingly, Radius seems to be well capitalized at around 2.6B$. That's from feb 2021, whereas they only had about 1.4B$ at the time of the close. So it's either Radius is an extremly fast growing bank or the stimulus checks are just filling up the coffers.

In summary, at current trajectory, we can assume $LC should have about 3B$ in deposits and about ~800M$ in assets. $JPM stands at 1.9 Price/Book Value (P/BV) and $WFC is closer to 1 P/BV. If we use a conservative multiple of 1 for P/BV this brings us to a target price of ~33$. I think it is possible once investor appreciate the innovation/disruption of API banking to give higher multiple (like Sofi/ $IPOE has). Therefore a P/BV of 2 is very likely which brings us to a target price of ~70$.

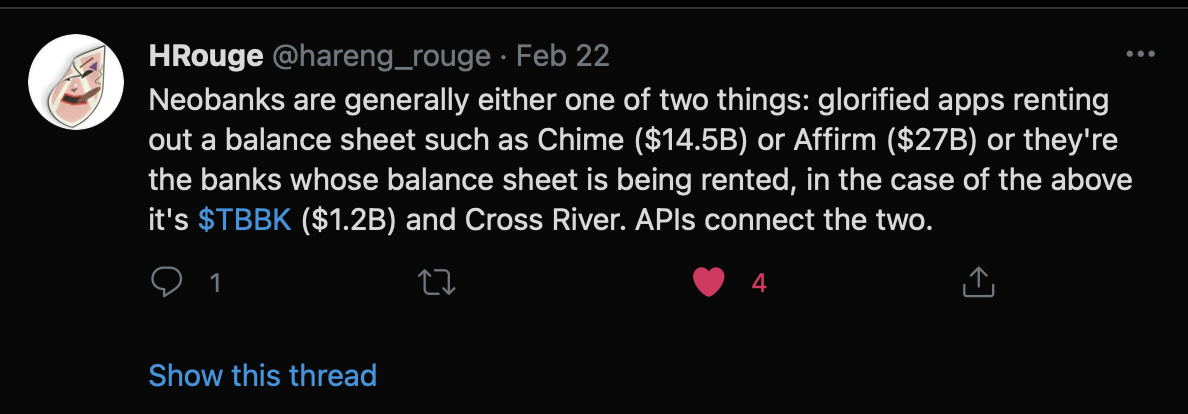

An interesting tweet from HRouge about how fintech as either one of 2 things:

- Glorified app renting out balance sheets (Chime 14.5B$ or Affirm 27B$ )

- Bank renting out a balance sheet $TBBK (1.3B$)

But what makes $LC unique is that they are now both. Both a bank (with a balance sheet) and a glorified app (the legacy Lending club business).

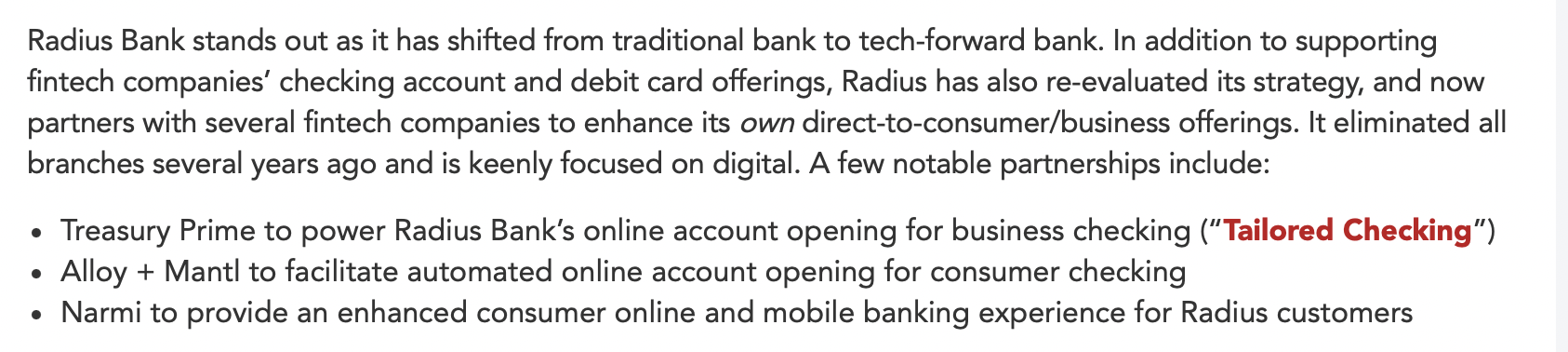

From this article, we learn that :

A few things to note, radius bank is using AlloyLabs and Mantl for online checking white label 1

We get more clarity on the radius bank numbers when the earnings are coming up on April 28th.

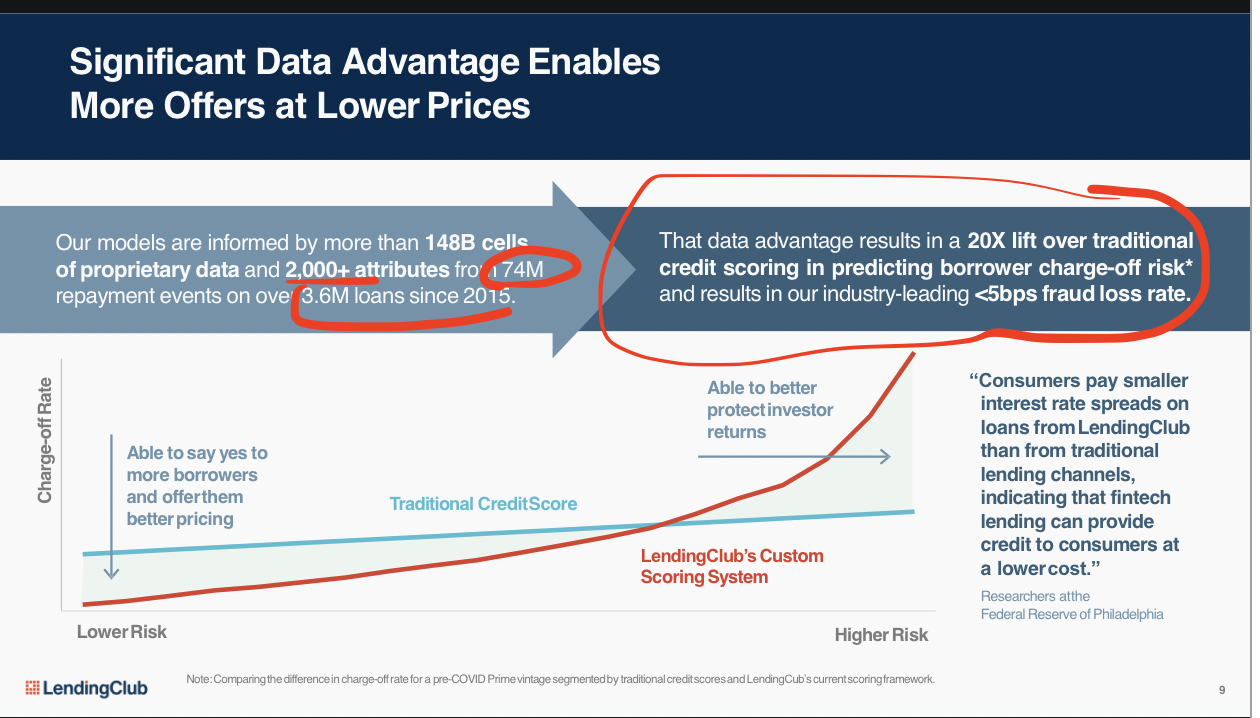

Moat 2: Data advantage

Lending Club CEO Scott Sanborn talked about it for the first time in the 4th quarter of 2020 as Lending Club having a data advantage. Most newer competitors tout their advantage as "better algorithms".

We cannot underestimate the power of machine learning and algorithms. If any of you had any experience with banks, they solely rely on the credit score for providing loans. This is quite pathetic for 2021.

The hypothesis here is that $LC can take advantage of it's current data to provide a better risk management than traditional bank can do.

To be honest, you don't need very fancy algorithms if you already have about 3M users. Having worked with machine learning algorithms for a long time, any practioners will tell you the data matters the most, and $LC have tons of it. Someone could argue traditional banks have even more, but there is a big structural and organizational step to go from a software company to a traditional bank. Therefore, I believe $LC is at the sweet spot where it is still ran as a Software company with plenty of loan data.

With moe data, you can simply track a few basic things and look up their behavior history as previous borrower. I would argue that those platform and data provide a lot more granularity than a typical fico score. Especially, having that data advantage will allow to price loan better than any traditional banks or other fintech. Take Sofi ($IPOE 8.5B$ post-money) as an example, they build their whole business on the fact that they would also look at your degree and grades (and not just your credit score). This gave them a huge hedge to provide cheaper and more secure loans.

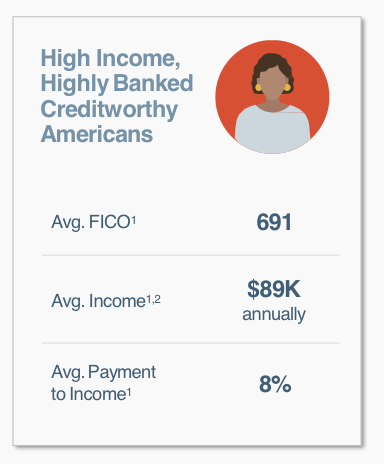

The other interesting information we got from the earning call is that the typical user of lending club tend to be high-income. It turns out, they also have higher debt. I suspect this is a similar demographic that Sofi (IPOE) is going after.

$LC with the bank license, is one of the few fintech that are vertically integrated. They basically now owns the full stack for a personal loan experience :

- Personal loan web-app

- Mobile checking for users direct deposit (i.e.)

- Mobile deposit for loan repayment

From the earning, this is the part that gets the tech investor excited. Banking is a traditional industry that is ripe for disruption.

$LC loan perfomance is 20x better (acccording to the management) than typical FICO scores. I entirely believe this, since I used to be have a very low FICO scores and I also once lost 100 points on my FICO score due to a 25$ subscription fee on a supposedly closed credit card. Bottom line, my personal experience is that FICO is shit. But more importantly, this shows that there is a virtuous cycle of data superiority providing a better product, which is my main argument that $LC is winner take-all platform. And lending could in fact also become a winner take-all market with 1 or 2 main companies. Likely banks are too slow to adapt for this, so $LC seems to have a shot at it since it is the leader. Another contender in my opinion is $IPOE.

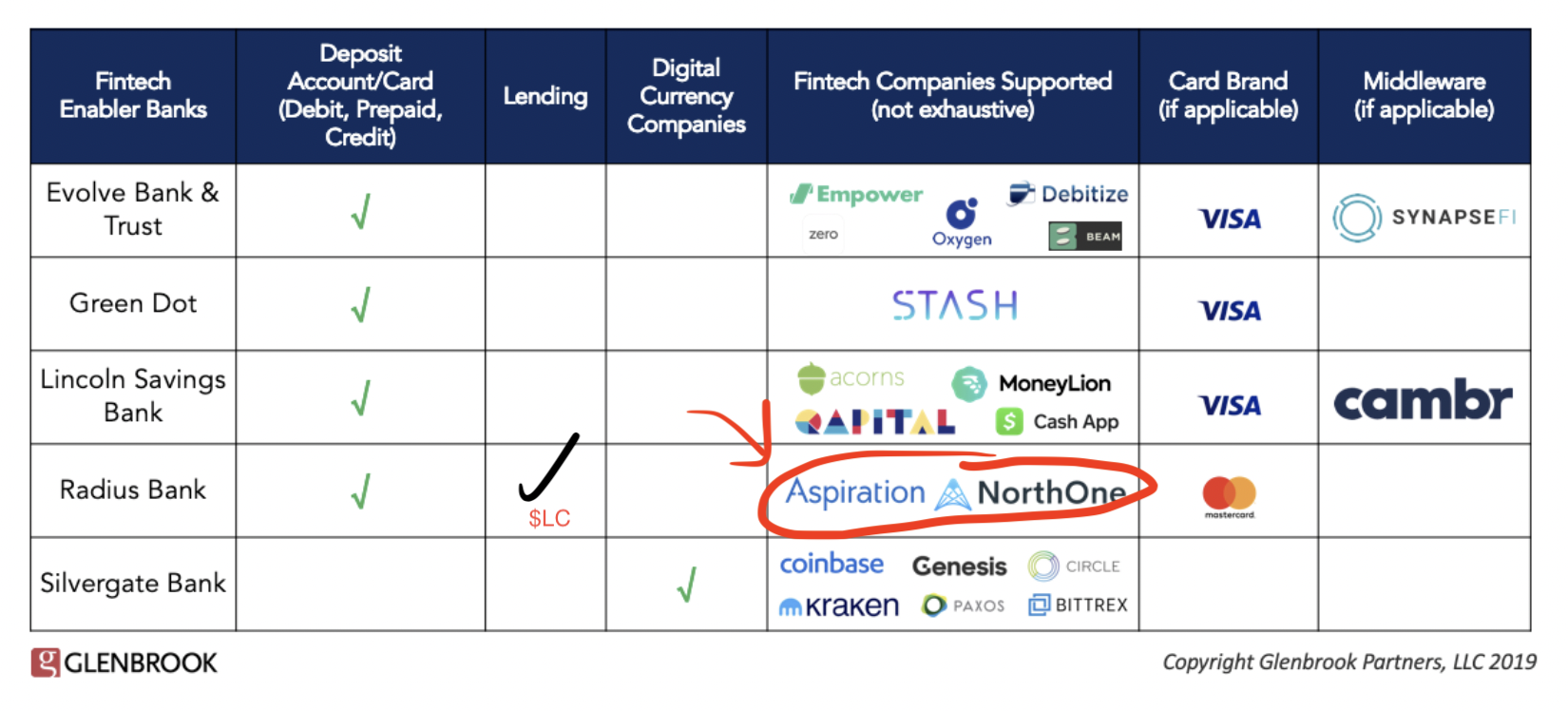

Moat 3: MarketPlace

Being marketplace or more generally platform is a winner take-all. There are no doubts about this. Look at Airbnb, Amazon, Google, Facebook, Uber, etc... those are all winner take-all where the bigger the platform, the more supply you have, the better the product and experience is for the users.

Glennbrook partners have a nice table in 1. If $LC+ Radius are able to fill up the "fintech" column, then this where it creates the moat.

Diversify income streams

From the earning call, $LC is intending to keep about 15-20% of loans originated for interest income and sell the rest through marketplace. This will allow :

- Interest income

- Capital light originations fees/ marketplace fees.

This will also allow $LC to serve more diverse population with other fintech/banks taking the lending risks. $LC will benefit by being the platform consumer interface with.

Loans offer with other fintech:

The power here is combining Moat 2 and Moat 3 to provide users with loans offers. For example, a high income person with bad credit (such as recent immigrant with STEM degree). By using radius as their online bank and taking a loan with Lending Club, $LC could potentially use my previous loan repayment, look for patterns in my checking account, the type of expenses I do, the list goes on, etc... That would give an hedge to Lending Club to provide me a better priced loan and at lower risk for $LC as opposed to a bank that would only look at my credit score.

Acquisition cost:

One amazing thing that $LC was able to prove is that it is able to provide very low acquisition cost. This is similar to what is happening with Airbnb where they stopped all customer acquisition expenses and are only focusing on the current user base. $LC could be close to that scale with 3M+ users. And if $LC can prove they provide better loan terms, users will organically flock to it.

Here's the direction I think $LC could take. Treasury Prime recently partnered with radius bank to provide business checking. Treasury Prime is the poster child of a fintech leveraging bank APIs. They are Y-combinator startup focusing on a particular vertical. If lending club leverage their current platforms with the 3M+ users, they could allow similar fintech underwriting loans for particular demographics, etc.. assuming they have better data or understanding of that target. This creates 2-sided marketplace with winner take-all dynamics and makes it very hard to replicate. This is still speculative at this point, but the CEO pointed at this direction in his blog.

Other concerns

A lot of people got burned by Lending Club and especially in 2016 when the fraud allegations came out. The ousting of the founder didn't help and the decade long decline in market capitalization was direct result of this. But I believe this era is behind us now and $LC is about it pivot it's business. The product itself (personal loans) were still very popular and provided a lot of benefit to it's users even during this tumultuous period.

Peer-to-peer is dead

That's the unfortunate truth: Peer-to-peer lending is bad business model and is dead. $LC management confirmed that when they shutdown all the individual investor notes in December 2020 and now the only investors left are institutional or funded directly (through radius).

Marketing cost

When analyzing companies, the best companies are the ones that need no marketing to bring back their customers. $LC seems to be one of them, since they simply slashed all the marketing costs during the pandemic and even though origination when down drastically, they maintained relatively well.

$LC also did a 30% personel cost.

Reopening play

Banks are the about the benefit greatly from the reopening after covid for the following reasons :

- Bank typically make money with steep yield curve. With Jerome Powell guaranteeing for rates to stay and inflation expectation picking up (high end of the yield curve), this is the perfect environment for bank to outperform the market.

- Banks are not getting the defaults everyone was scared about. Seems the Fed and Biden administration is determined to provide plenty of liquidity or just outright money.

- Economy re-opening, meaning people are spending money again and taking on debt for wedding, travel, housing, etc...

How to value $LC

The hardest question is how to value $LC.

- Is this a bank?

- Is this a tech company?

- Is this a marketplace winner take-all platform?

- How does $LC compare with other fintech valuations?

This is literally the $ billion dollars$ question. This is where us (the retail investor) can shine since we have 2 things in our advantage. One is time and the other is we have no career risk. It's my fucking money after all... no one can fire me, cancel me or dump my fund if I'm wrong. And just a reminder, this is NOT investment advice. I'm just a rando on the internet with no financial qualifications professing a love for a particular security $LC.

What if I'm still wrong??

My strategy is typically to study a company and try to understand business from a operator/technologist point of view. When I'm wrong (and if my investment is down significantly), I typically go back listening and reading about the earnings and the business and try to see if Mr Market is just acting crazy (or not). Companies do get mispriced a lot and I don't personally believe that efficient market theory applies ALL the time. But it eventually converges to a fair(er) value. Our opportunity is to find those mispricing. I found that in turn-around companies (especially tech + turn around companies), most analysts are lost and there are lot of upside gains. Gamestop ($GME) was one great example. I strongly believe $LC (Lending Club) could have a similar outcome.

Valuing as a tech company

A typical tech company growing revenues yoy 30%+ can easily trade a 10-20x multiple of revenues if it is a simple business like SASS with recurrent revenues.

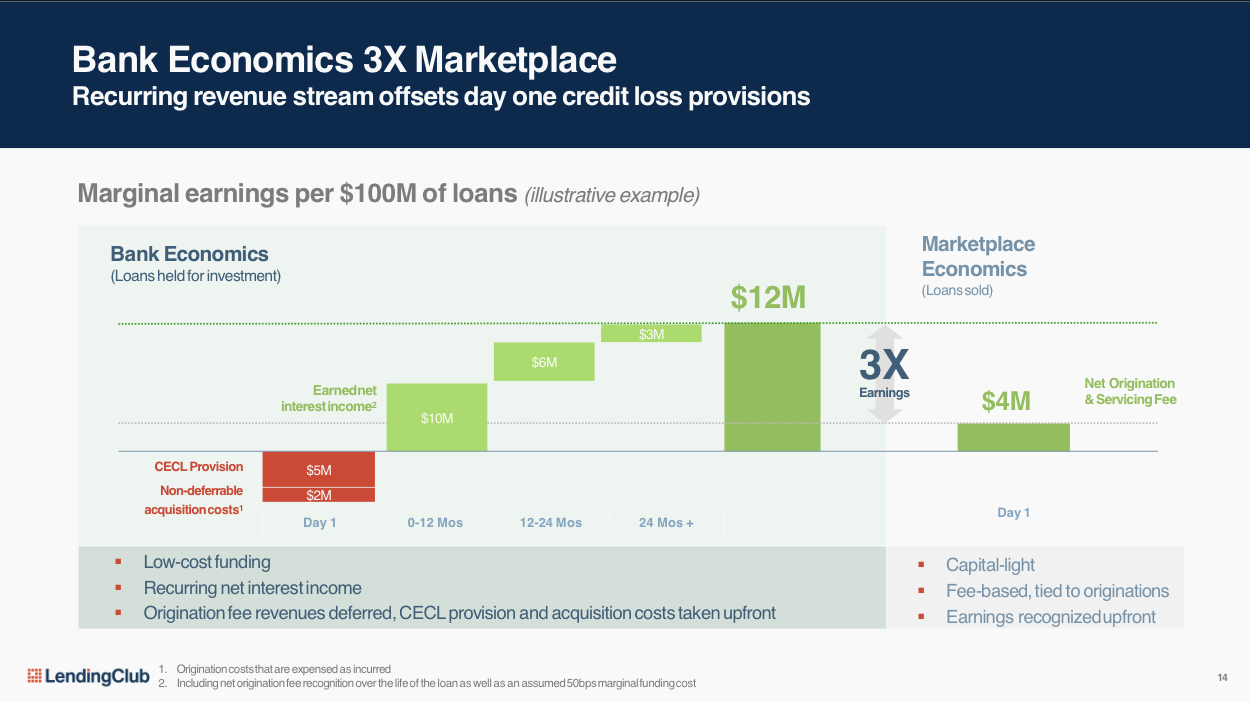

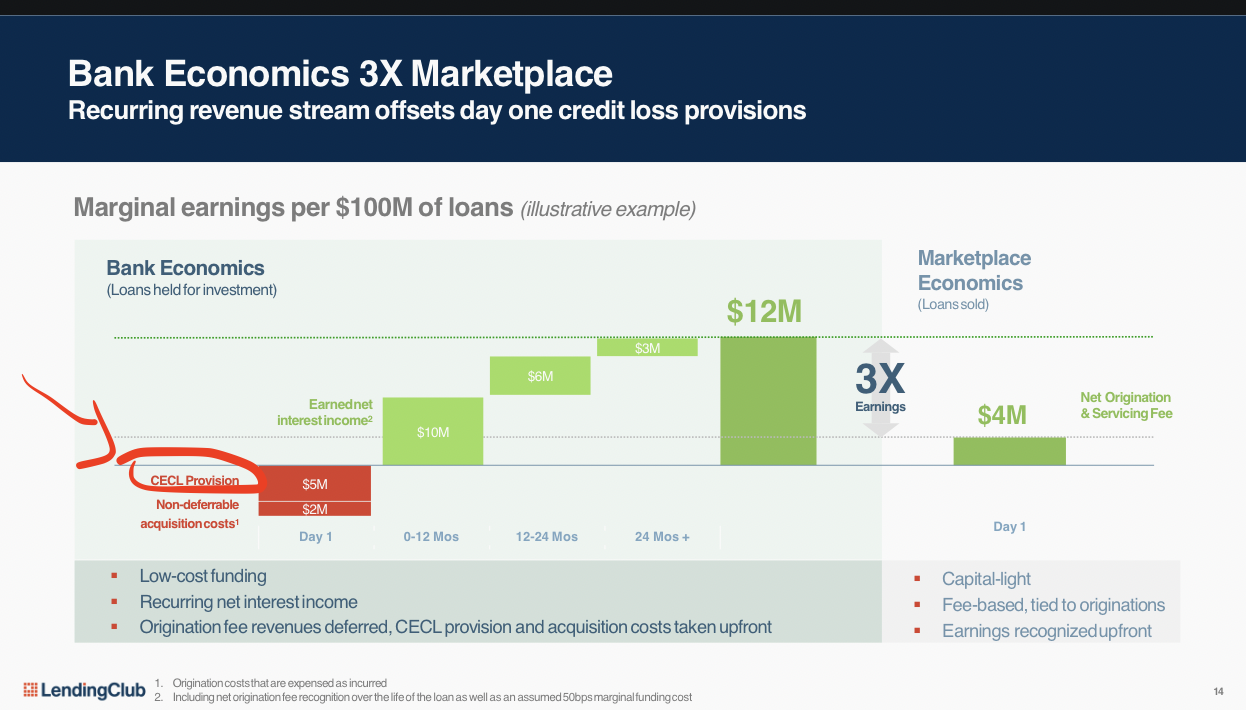

One interesting note we got from the earning call is that $LC will hold loans on the balance sheet which will provide recurrent income stream.

Every 100M$ of loans will generate 12M$ of income. This also breaks the 1 to 1 relationship between loans and origination. So this means, origination can go down and $LC can stil generate plenty of recurrent revenues with the loans.

Also most the GAAP loss for FY2021 is due to CECL. This means $LC need to account for loss provisions upfront for adding the new loans to it's balance sheet. However, if the theory holds and that AI/Machine learning provide less risk, this will create a good money printing machine. So as long as $LC is growing, expect to get GAAP net loss due to those CECL provisions.

Competitions

There are 2 companies that are closest to $LC model but neither are exactly as fully vertially integrated as $LC.

- SOFI ($IPOE): Valuation of 8.5B$. This is the SPAC from Chamath. They are just starting the bank application process and will likely take more than 1 year for it to happen. They offer un-secure loans like $LC but also offer mortgages and investment options.

- Revenues : 620M$ (2020)

- 1.7M Users

- Valution : 8.5B$

- Chime : Is a typical fintech startup. This provides an idea about what Radius can execute and become.

- Revenues : 500M$+

- 8M+ Users

- Valuation: IPO around 30B$ 7

Lending club has an enterprise value of around ~1.5B$ (as of March 22nd) along with about 2B$ deposits.

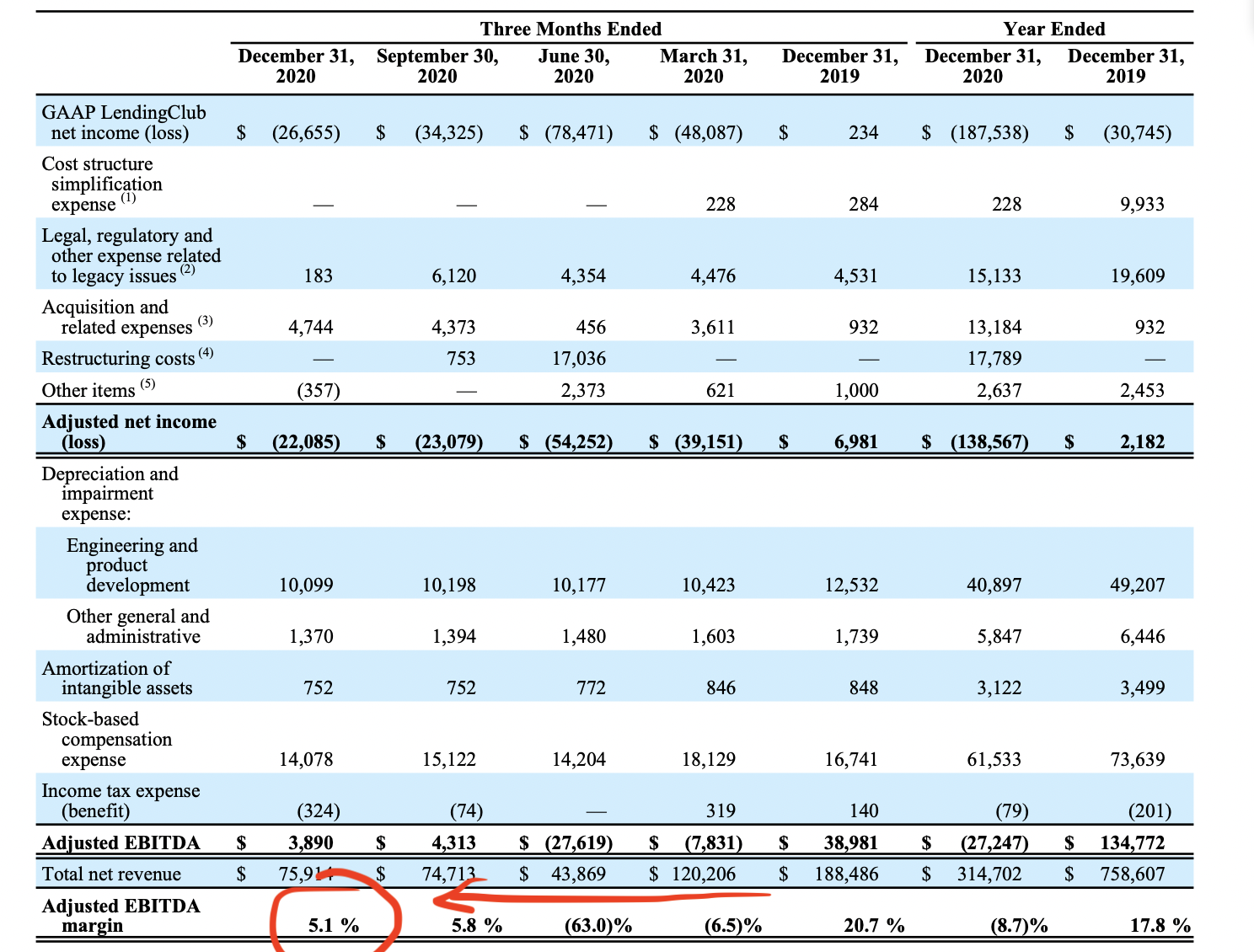

** EBITDA Positive **

I know that Warren Buffet hates this metric, but it does provide a good direction of where the business is going.

They were able to generate 5% of EBITDA margin out of ~75M$ in revenues for Q4 2020.

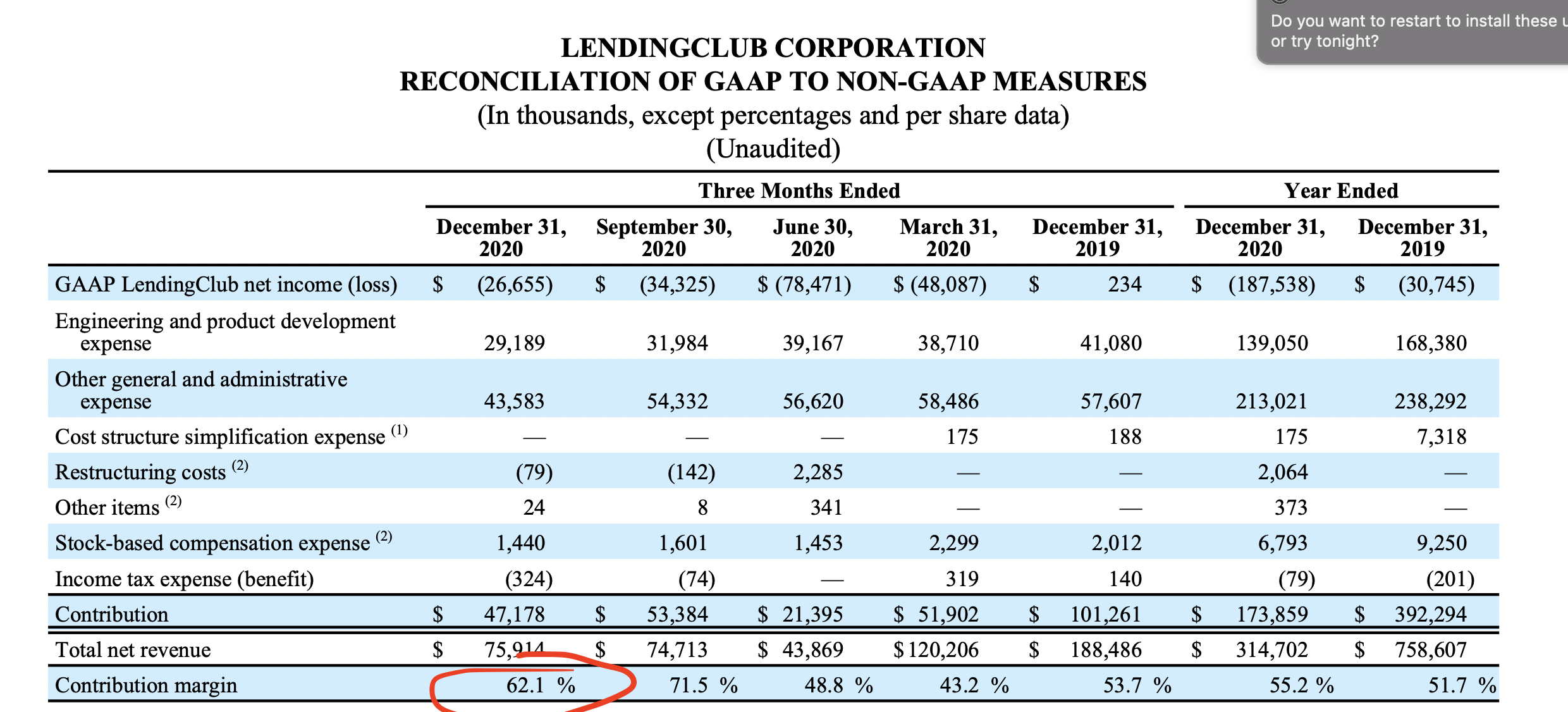

Contribution Margin

The other notable metric to follow is the growth in contribution margin. This also provides an idea about future profitability once the acquisition is completed and reopening fully kicks in.

Insider buying

One interesting note is that the CFO (Casey Thomas) bought some more $LC, raising his stakes by 5%. There has been a lot of selling from other exec, but it seems to looks like more cashing out (for daily expenses) than giving up on the business.

Conclusion

In my opinion, the market is not giving enough credit to the turn around for Lending Club. There are still some risks ahead but mid to long term, I believe $LC has the potential to be quite profitable. There are a few cataclysts coming in the next few months namely:

- Full numbers from radius banks

- Reopening play and interest rates likely continuing their trend up.

Stay long here.

Subscribe to Be free and wealthy blog

Get the latest posts delivered right to your inbox